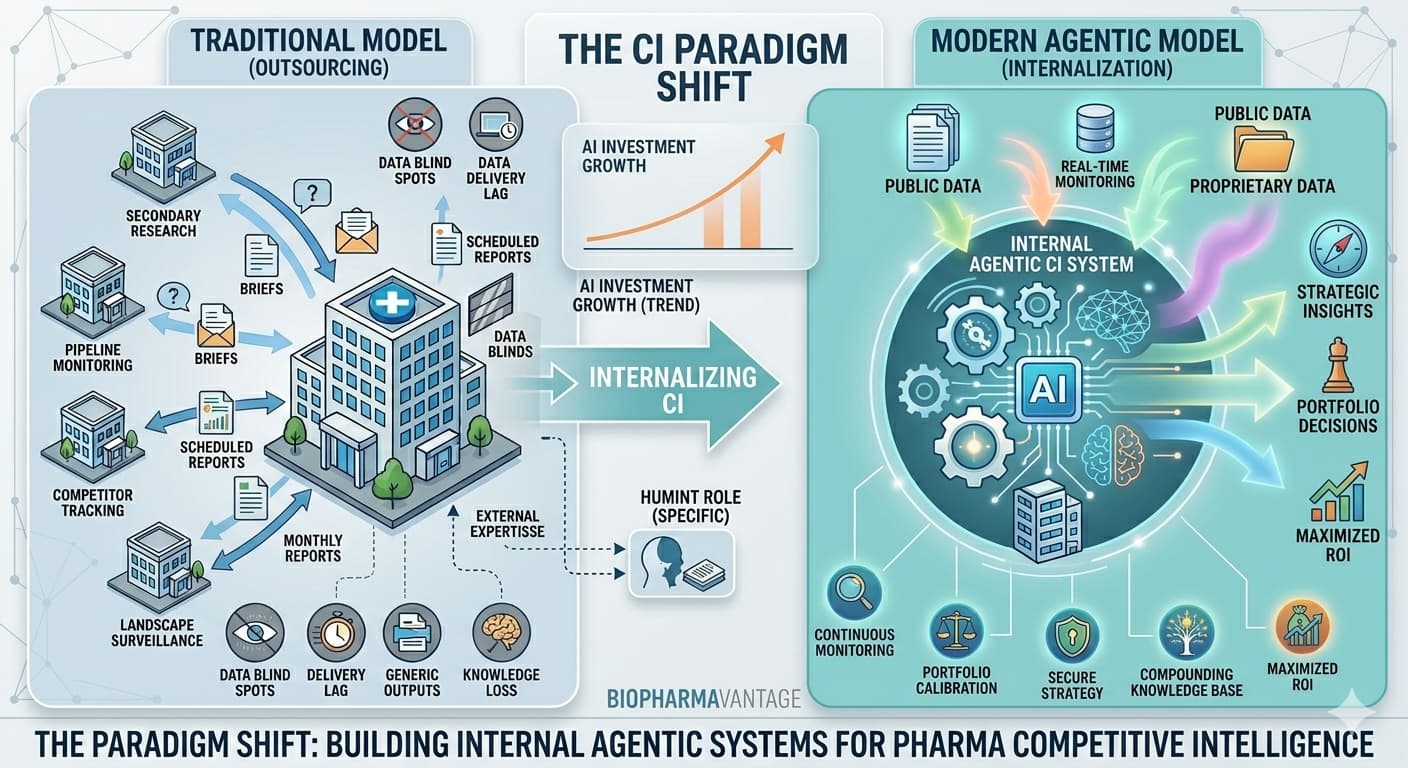

Why Biopharma Companies Are Switching to Internal AI-based Agentic Competitive Intelligence Systems

For decades, the biopharmaceutical industry has been reliant on pharma competitive intelligence vendors for secondary research and monitoring to meet its competitive intelligence (CI) needs. The logic was straightforward: vendors brought specialist expertise, access to data and intelligence, and analytical frameworks that internal teams could not justify building from scratch. For most of that period, this model made perfect economic and operational sense.

However, the calculus has fundamentally changed. Leading pharma organizations are dismantling the legacy model, phasing out external vendors for secondary research in favor of building internal agentic AI-based competitive intelligence systems. The emergence of agentic AI – autonomous systems capable of monitoring, analyzing, and synthesizing intelligence continuously and at a negligible marginal cost – has removed the core rationale for outsourcing routine secondary pharma CI and monitoring programs.

This does not mean external expertise has no role in pharma competitive intelligence – primary research, i.e., HUMINT, remains an area where external partners add genuine value that AI cannot replicate. But for secondary research, pipeline monitoring, competitor tracking, and landscape surveillance – the bread and butter of most pharmaceutical competitive intelligence vendor relationships – the argument for outsourcing has largely collapsed. Here are ten reasons why.

1. External Pharma Competitive Intelligence Vendors Are Permanently Blind to Your Most Valuable Data

The most significant competitive intelligence a pharma company possesses is not publicly available. Your internal trial outcomes, failed development programmes, real-world evidence datasets, manufacturing cost structures, and the intelligence gathered through your own primary research represent a proprietary analytical layer that no external vendor can access – nor should they.

This is not a minor limitation. It means that vendor-produced secondary pharmaceutical competitive intelligence is assessed entirely in isolation from the context that makes it strategically actionable. A competitor’s Phase 3 readout means something very different when evaluated against your own confidential data on a similar programme than it does when assessed in isolation against public benchmarks. An internal agentic CI system can make this correlation. No external vendor can. As we describe in our guide to pharmaceutical competitive intelligence, the most powerful CI outputs emerge at the intersection of public signals and proprietary context – a synthesis that is structurally impossible when pharma CI outsourcing is the operating model.

2. Every Brief You Send a Vendor Exposes Your Strategic Intent

In pharmaceutical competitive intelligence, what you ask is as sensitive as what you find. Every monitoring brief, every ad hoc deep-dive request, every competitive landscape commission sent to an external vendor reveals something about your strategic priorities, your concern areas, and the decisions you are considering.

Asking a vendor to investigate a specific competitor’s CNS pipeline signals that you are evaluating a competitive threat. Requesting intelligence on a particular geography or regulatory pathway signals a market entry consideration. Reputable vendors maintain confidentiality, but the structural reality is that your strategic intent is being shared with a third party – one that may serve your direct competitors using the same analysts, the same platforms, and in some cases the same frameworks possibly, after a cooling-off period An internal agentic system, operating entirely within your secure infrastructure, ensures that your pharma competitive intelligence interrogation never leaves the corporate firewall.

3. The Economics of Pharma Competitive Intelligence Externalization No Longer Make Sense

Traditional pharmaceutical competitive intelligence vendor relationships operate on an OpEx model structured around recurring fees – annual monitoring programmes, per-project charges, and FTE-based fees. The cost scales roughly linearly with coverage: more therapy areas, more competitors, more geographies means proportionally more expenditure. This creates budget constraints that force prioritisation and inevitably leave intelligence gaps in areas that do not make the cut.

AI investment in pharma is expected to grow significantly – a trajectory driven precisely by the recognition that once internal AI infrastructure is operational, the marginal cost of expanding coverage approaches zero. Monitoring 100 competitors instead of 20, covering 50 indications instead of 10, tracking 200 data sources instead of 30 – none of these expansions require proportional cost increases in an internal agentic system and is a key to unlocking value and performance. You are building a permanent strategic asset rather than perpetually procuring a service. The long-term ROI differential between these two models is substantial and is one of the most ingenious ways for maximising the ROI of competitive intelligence engagements.

4. Institutional Knowledge Walks Out with the Pharma Competitive Intelligence Vendor

One of the least discussed costs of outsourced pharma competitive intelligence is the institutional knowledge that accumulates inside the vendor rather than inside your organisation. A vendor team that has monitored your therapeutic areas for three years develops a deep understanding of the competitive landscape, the key signals worth tracking, and the analytical patterns that predict meaningful developments. When the contract ends – or when a key analyst moves on – that accumulated intelligence leaves with them. This is further augmented when there are changes in the internal teams as well. Your programme resets.

An internal agentic CI system builds a compounding knowledge base that deepens over time. It learns your portfolio, your strategic priorities, and your competitive history. Each cycle of intelligence gathering enriches the system’s understanding of what matters to your organisation specifically. This compounding effect – institutional memory that accumulates rather than resets – is one of the most undervalued advantages of internalising pharma competitive intelligence, and one that becomes more significant the longer the system operates.

5. Vendor Delivery Cycles Are Structurally Incompatible with Real-Time Pharmaceutical Competitive Intelligence

The standard deliverable model for external pharma CI – alerts emails, weekly or monthly reports, periodic deep-dives – was designed for a competitive environment that no longer exists. While competitor data readouts, regulatory decisions, patent filings, and deals announcements are covered by vendors’ alerts, technically, they are not with you in real-time to you – there is always a lag.

Teams that previously managed ten strategic analyses each month can now address dozens of business questions using agentic AI, compressing analysis from weeks to minutes – a speed advantage that is structurally impossible within a vendor relationship dependent on human analyst bandwidth and project delivery workflows.

In markets where a competitor’s Phase 2 readout or a regulatory approval can shift portfolio priorities overnight, an intelligence lag in pharma competitive intelligence outsourcing is not a minor inconvenience. It is a material strategic risk that compounds across every competitive event in a given year. Vendors can claim to use agentic AI as well, but why won’t you have it internally? The cost to procure and establish such a setup is often less for the pharma client than it is for a vendor.

6. Generic Vendor Outputs Are Not Calibrated to Your Portfolio

External pharmaceutical competitive intelligence vendors design their products and frameworks for broad applicability across multiple clients. A standard competitive intelligence report is built to be useful to any company operating in a given therapeutic area, which means it is optimised for no company in particular but is often tweaked to meet your needs. The analytical lens is generic, the signal prioritisation reflects average relevance across a client base and vendor understanding, and the strategic interpretation is generic.

Your competitive threats are not generic. They are evaluated through the specific lens of your asset mix, your pipeline stage, your commercial position, and your strategic priorities. A competitor’s regulatory filing in a rare disease indication has a completely different strategic significance depending on whether your own programme is in Phase 1, Phase 3, or already on market. An internal agentic pharma CI system can be configured to apply exactly this portfolio-specific analytical filter. Vendor products cannot, without bespoke configuration, thereby reintroduces increased cost, delivery latency and externalization risks.

7. AI Has Eliminated the Technology Advantage That Justified Pharma CI Outsourcing

The primary historical argument for outsourcing secondary pharmaceutical competitive intelligence was ‘value’ primarily driven by therapy area expertise and cost-effectiveness. That argument has been substantially dissolved by the democratisation of agentic AI.

Several pharma companies now view AI application as an immediate priority, a position that reflects widespread recognition that the technology required to build in-house pharma competitive intelligence capability is now accessible, eliminating vendor dependency. Internal teams can deploy natural language processing across the same public data sources vendors use, build monitoring workflows across clinical trial registries, patent databases, and regulatory filings, and configure agentic systems that continuously synthesise outputs – all without the overhead, margin, and strategic dependency of a vendor relationship. The technology moat that justified pharma competitive intelligence outsourcing has largely been filled.

8. Multi-Client Vendor Exposure Creates a Structural Conflict of Interest in Pharma CI

Reputable pharmaceutical competitive intelligence vendors maintain ethical walls between client engagements. The conflict of interest is nonetheless structural and should be understood clearly. The same vendor serves multiple pharma companies, often including direct competitors in the same therapeutic areas. The same analysts, the same data infrastructure, and the same analytical frameworks serve organisations on opposite sides of the same competitive battle.

This is not an accusation of misconduct — it is an observation about structural reality. The analyst who monitors a competitor’s oncology pipeline for your organisation this quarter may have built the framework that monitors your pipeline for a competitor last year. The patterns and methodologies that generate your pharma competitive intelligence are not proprietary to you under an outsourced model. They are shared assets deployed across a client base that includes your adversaries. Internalising CI eliminates this exposure entirely.

9. Outsourced Pharma Competitive Intelligence Arrives as a Deliverable, Not a Decision Input

There is a fundamental difference between pharmaceutical competitive intelligence that readily supports decision-making and intelligence that acts as a precursor for decision-making. External vendor CI predominantly arrives in the second category – as a formatted deliverable, delivered on a schedule, consumed by a CI team that then translates it into internal decision inputs. This translation step introduces delay, interpretation variance, and disconnection from the specific decisions the intelligence should be driving.

Internal agentic pharma CI is embedded directly in decision workflows. It feeds planning processes in real time, surfacing relevant intelligence at the moment decisions are being made rather than between decision cycles. CI that cannot be connected to a specific decision is not generating strategic value regardless of its analytical quality. The workflow integration that transforms pharmaceutical competitive intelligence from a deliverable into a decision input is structurally easier to achieve with internal systems than with external vendors.

10. Pharma Competitive Intelligence Externalization Forfeits the Capability Development That CI Work Generates

The analytical skills, domain knowledge, and institutional memory that competitive intelligence work generates are not merely outputs – they are organisational capabilities that compound in value over time. When secondary pharma CI is externalized, these capabilities accumulate inside the vendor rather than inside your organisation. Your internal CI function becomes a client of expertise rather than a generator of it.

Pharma companies lacking deep in-house AI and CI expertise struggle to fully unlock AI’s potential—a gap widened, not narrowed, by a sustained reliance on outsourcing core CI work. Building internal pharmaceutical CI capability – comprising teams that understand both the competitive landscape and the agentic systems monitoring it – develops the ‘strategic muscle’ that will differentiate CI leaders from followers. By outsourcing pharma CI, companies risk becoming structurally dependent on pharma competitive intelligence vendors just as in-house intelligence capability becomes a key source of competitive advantage

BiopharmaVantage provides specialist competitive intelligence, primary research and HUMINT, strategic analysis and benchmarking, and licensing and partnering services to pharmaceutical and biotechnology companies. To discuss how we can support your competitive intelligence needs, contact us.